Beyond borrowing: How women in Tangail make sophisticated investments

“Cattle, savings, and hard work keep my household standing,” remarks Mita Ghosh, a BURO member for more than a decade.

Mita joined the microfinance institution (MFI) BURO soon after she got married. Her mother-in-law was already a member and brought her to a BURO meeting. At her first session, she learned why saving matters and began to put aside BDT 20 (~USD 0.16) each week.Over time, she took her first loan for BDT 67,000 (~USD 546). The loan helped her buy a calf and support the household. She repaid the loan, borrowed again,and repaid that loan amount, too. She repeated the cycle until she no longer needed loans.

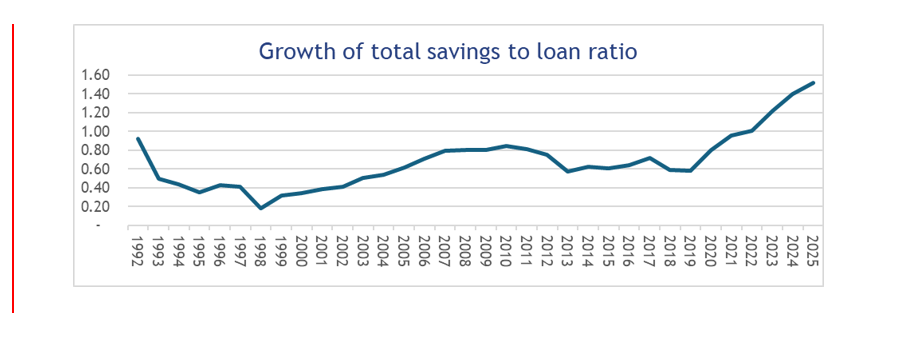

Institutions, such as BURO Bangladesh, have helped expand financial inclusion for their low- and moderate-income members by building savings habits early. Around 30 years ago,BURO removed mandatory savings, on the view that forced savings do not create voluntary discipline.

Currently, in the five model BURO branches,savings have outgrown borrowing, and members save consistently and choose when to borrow and when to rely on their own savings . The members built financial acumen through periodic financial literacy camps and knowledge-sharing sessions . Members could choose savings products that fit their needs.

Source:BURO’s historical branch-level data

A BURO branch manager noted, “They educated their children, who are now well-established. These families are now solvent and self-sufficient. Their need for loans has decreased, and their capacity to save has increased.” The accounts from our field visit echo this statement.

Ratna from Dawli branch joined as a member 15 years ago. She has saved more than BDT700,000 (USD 5,700) through consistent weekly deposits. She farms and rearscattle to support her family and borrows only when necessary. Meanwhile, Mina from Atia branch owns five cows and plans to acquire two more. She took a loan last year to build a bigger cowshed and has repaid it in full.

Begum runs a grocery shop, which she built entirely from her own savings. She paid for her three daughters’ weddings without borrowing money. She still maintains an active Deposit Pension Scheme (DPS) account for her son’s future. Similarly,Aruna from Pathrail saved consistently for 16 years. She began with just a BDT5,000 (~USD 40.67) loan and a BDT 500 (~USD 4.07) monthly DPS. Over time, she motivated her whole family to save. After years of saving, the family funded their daughter’s education, marriage, and resettlement.

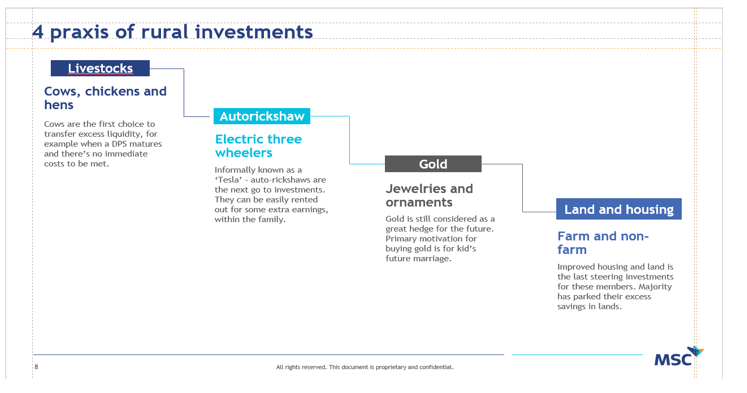

We saw the same progression across several BURO branches in Tangail. Members borrow early to get established, then gradually shift to saving, with credit that becomes something they use by choice rather than necessity. Typically, well-established BURO members invest in four things: Livestock, electric autorickshaws, gold, and land.

Abranch who has been working there for the past 16 years have shared that he has seen families who have saved in BURO and used that money to educate, marry and settle an entire family of their daughter whereas one day this particular customer had took a 5000 taka loan and 500 taka DPS, Just an example

The first two of these investments yield regular income and can be managed from the homestead. Cows are a great asset, as highlighted by Stuart Rutherford in his book The Poor and Their Money. Livestock has practical limits: Most households can keep about five cows and a few more chickens due to space constraints. Cows are especially valuable because milk sells reliably.

Electric autorickshaws are popular investments. Women often buy one and rent it out,usually to a family member between school and work or to someone looking for a job. Another important investment is gold. In Bangladesh, gold functions as an appreciating, portable, and liquid asset. Gold is a store of value and a key requirement for marriage, especially for the daughters of members.

Across Dawli,Atia, and Pathrail branches ,women run 10-year DPS accounts earmarked for their daughters’ jewelry. Mukta Begum has two accounts to buy gold: One in her own name and one in her daughter’s name. One member in Dawli branch encashed a 10-year DPS the moment it matured and went straight to a goldsmith. The next DPS account she openedwas for the same purpose but for a different daughter.

Land is the next big investment. Our research also found that most long-term members buy a plot, either farmland that they rent out at harvest or land near town. It takes more capital than one DPS cycle, is hard to cash out quickly, and comes with legal hassles. However, land is where members park money once they have built a base.

Based on land ownership, some members invested in the agriculture sector, either directly in production or in the pre- and post-production value chain. This pattern of investment has created massive expansion in this sector. It has also led to a rise in the diverse field of borrowing and saving in various agricultural businesses and products, such as livestock fattening, aquaculture, and seed banking. This expansion has created an opportunity, especially for women, to invest financially in a sector that significantly contributes to the country's economy.

A BURO’s branch managers shared, “They educated their children, who are now solvent and well-sufficient.”

This initiative, along with small investments in microfinance institutions such as BURO, has expanded the availability of various agricultural products and businesses nationwide. It has secured food security and created income-generating opportunities for people in the marginalized communities. The initiative also helped people save for their future and become financially independent.

The agricultural crop map shows that agricultural products have expanded in each zone, and where BURO’s clients have invested most. For example, most clients who take seasonal loans in Rangpur use them for rice or potato cultivation or for work in those sectors. In Rajshahi, the majority of seasonal and agricultural loans relate to mango cultivation and grain harvesting.